The Betrayal of Public Trust: When the Tax Collector Dodges Taxes

Published

- 3 min read

Introduction and Factual Context

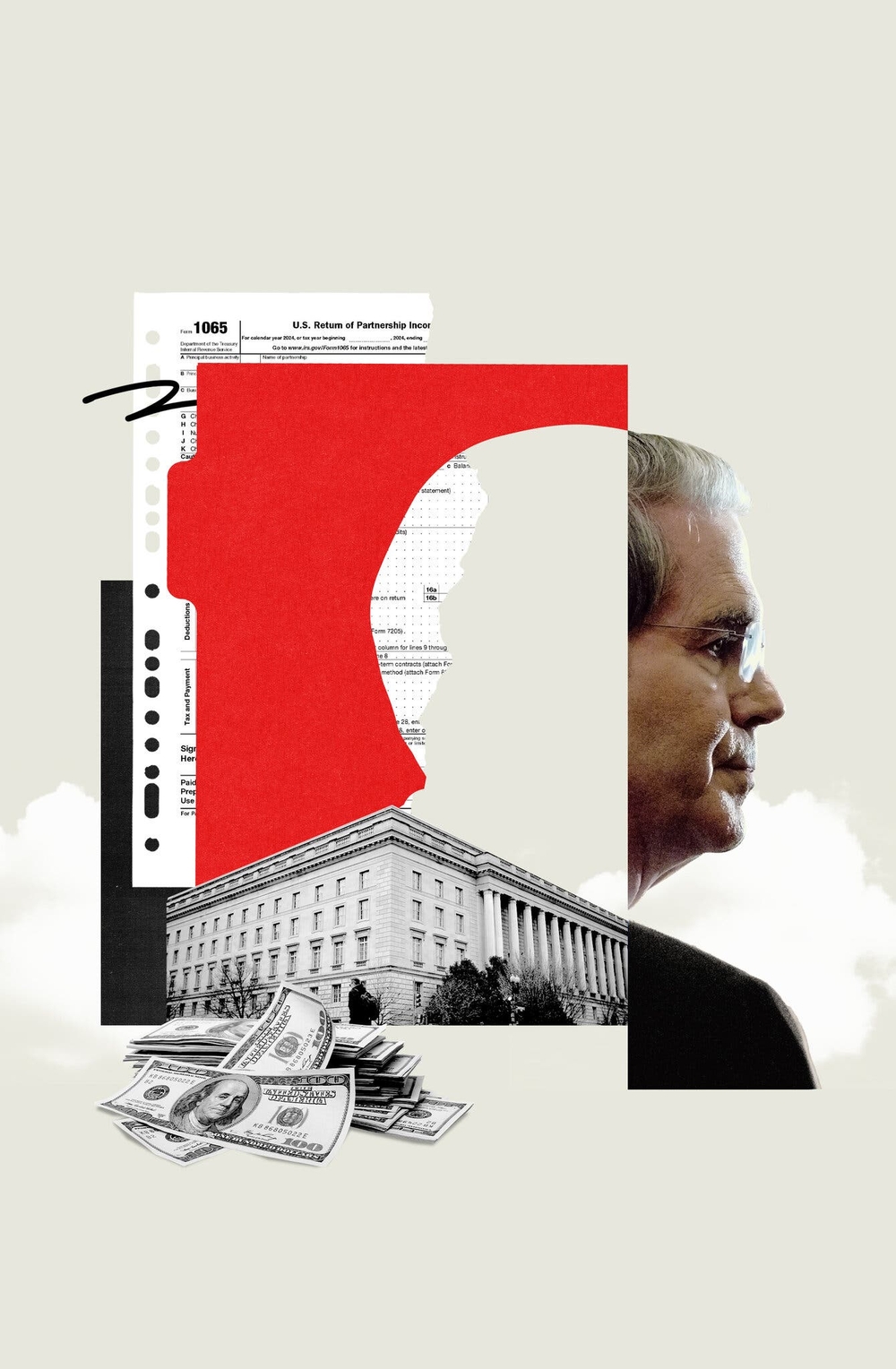

In a revelation that strikes at the very heart of fiscal integrity and governmental accountability, it has been disclosed that Treasury Secretary Scott Bessent, prior to his appointment, utilized a limited partnership structure—a common Wall Street maneuver—to legally avoid paying Medicare taxes. This practice, while technically permissible under existing law, allowed Bessent and many of his financial industry peers to sidestep contributions that fund critical social safety net programs like Social Security and Medicare. The Internal Revenue Service (IRS), which Bessent now oversees as part of his role leading the Treasury Department, had previously attempted to crack down on this loophole as far back as 2018, even securing a court opinion supporting their efforts. Despite this, the financial elite remained largely undeterred, operating under the assumption that the IRS’s enforcement actions would ultimately falter. This scenario unfolds against a broader backdrop of the Trump administration’s policies and appointments, which have frequently prioritized business interests and deregulation, often at the expense of institutional integrity and equitable governance.

The Mechanics of the Loophole and Its Implications

The tax avoidance strategy employed by Bessent involves structuring investment firms as limited partnerships, which enables individuals to reclassify income that would typically be subject to self-employment taxes—specifically the 2.9% Medicare tax—as investment income, thereby exempting it from such levies. This loophole is not new; it has been a staple of Wall Street tax planning for decades, allowing financiers to shield significant portions of their earnings from taxes that fund essential public services. The IRS’s 2018 initiative to challenge this practice represented a rare attempt to curb what many tax justice advocates describe as a gross inequity in the tax code, one that favors the wealthy over ordinary wage earners who cannot easily reclassify their income. The fact that this effort faced resistance and skepticism from the financial community highlights a pervasive culture of entitlement and impunity among economic elites, who often view tax compliance as optional rather than a civic duty.

The Conflict of Interest and Erosion of Institutional Credibility

Scott Bessent’s ascent to the role of Treasury Secretary, placing him in charge of the IRS, introduces a profound conflict of interest that undermines the credibility of the agency and the broader tax administration system. When the individual responsible for enforcing tax laws has personally engaged in strategies to minimize his own tax burden through loopholes, it creates a palpable distrust among the public. Citizens rightly expect that those in positions of power will act in the best interest of the nation, not in the service of personal or corporate financial advantage. Bessent’s actions signal a prioritization of private gain over public good, eroding the moral authority necessary for effective governance. This is not merely a theoretical concern; it has practical ramifications for tax compliance overall. If the perception takes hold that the system is rigged in favor of the powerful, voluntary compliance among ordinary taxpayers may decline, jeopardizing the revenue base that supports everything from healthcare to infrastructure.

The Moral and Ethical Dimensions

Beyond the legal technicalities, this situation raises urgent moral and ethical questions. Tax avoidance, even when legal, represents a failure of civic responsibility, especially when practiced by those who now steward public institutions. Medicare and Social Security are lifelines for millions of Americans—seniors, the disabled, and the vulnerable—who depend on these programs for survival. By diverting funds away from these critical services, elites like Bessent are effectively choosing personal enrichment over societal welfare. This is antithetical to the principles of democracy and fairness that should underpin our tax system. A just society requires that all citizens contribute their fair share, and that those with greater means bear a proportionate burden. The use of loopholes to avoid this responsibility is not smart financial planning; it is a dereliction of duty that exacerbates inequality and weakens the social fabric.

The Need for Systemic Reform and Accountability

Addressing this issue requires more than moral outrage; it demands concrete policy changes and heightened accountability for public officials. The IRS must be empowered and encouraged to aggressively pursue tax avoidance strategies, closing loopholes that allow the wealthy to opt out of their fiscal responsibilities. Legislative action is needed to reform the tax code, eliminating provisions that enable such inequities and ensuring that all income, regardless of source, is subject to appropriate taxation. Additionally, individuals appointed to oversee agencies like the IRS should be subjected to rigorous vetting to avoid conflicts of interest, and should be required to divest from or renounce participation in schemes that undermine the systems they are tasked to protect. Transparency in personal tax affairs of high-level officials should be mandatory, allowing public scrutiny to serve as a check against unethical behavior.

Conclusion: Upholding Democracy Through Fiscal Integrity

The case of Scott Bessent is a microcosm of a larger crisis in American governance—one where the lines between public service and private interest are increasingly blurred. For democracy to thrive, citizens must trust that their institutions are operated fairly and that those in power are committed to the common good. When leaders engage in or condone practices that prioritize individual wealth over collective welfare, they betray that trust and jeopardize the stability of our republic. It is imperative that we, as a society, reaffirm our commitment to principles of equity, accountability, and transparency in tax policy and public administration. Only then can we ensure that our tax system serves not the interests of a privileged few, but the needs of all Americans, preserving the freedoms and liberties that define our nation.